The commercial real estate sector in the United States faces two structural forces that, at first glance, appear unrelated: the rapid expansion of data centers to support artificial intelligence workloads, and a persistent shortage of housing in major metropolitan areas. According to PGIM Real Estate's Cathy Marcus, these forces are converging in ways that reshape how investors and developers think about office buildings — and what those buildings might become next.

Marcus, who serves as co-head and global chief operating officer of PGIM Real Estate, discussed the dynamics on Bloomberg Television, pointing to the physical and infrastructural limits that data center construction is beginning to encounter and the growing momentum behind converting underutilized office space into residential housing.

Infrastructure constraints meet adaptive reuse

The AI data center boom has been one of the defining themes in commercial real estate over the past several years. Hyperscale operators and cloud providers have driven demand for facilities with enormous power, cooling, and connectivity requirements. But that expansion does not happen in a vacuum. Power grid capacity, water availability, permitting timelines, and land suitable for industrial-scale construction all impose hard ceilings on how fast and where new data centers can be built.

When those ceilings bind, the capital and strategic attention of real estate firms naturally shift toward other asset classes with strong demand fundamentals. Housing is the most obvious candidate. The United States has faced a well-documented shortfall in residential supply for over a decade, a gap widened by underbuilding after the 2008 financial crisis, rising construction costs, and zoning restrictions in high-demand markets. The mismatch between where people want to live and what is available to them has kept housing affordability at the center of policy debates at every level of government.

Office-to-residential conversion — often grouped under the broader concept of adaptive reuse — offers a partial answer. The idea is not new; cities have repurposed commercial buildings for decades. What has changed is the scale of opportunity. Remote and hybrid work arrangements, accelerated by the pandemic, have left vacancy rates in many central business districts at elevated levels. Buildings that once commanded premium office rents now face structural, not cyclical, demand declines. For owners weighing the cost of holding a half-empty tower against the economics of conversion, the calculus has shifted.

The practical limits of conversion

Not every office building is a viable candidate for residential conversion. Floor plate depth, window placement, plumbing infrastructure, and structural systems all determine whether a conversion is physically and financially feasible. Mid-century towers with deep floor plates and sealed facades often prove prohibitively expensive to retrofit. Conversely, older pre-war buildings and certain post-2000 structures with narrower floor plates and operable windows tend to convert more readily.

Municipal policy plays a significant role as well. Several major U.S. cities have introduced or expanded tax incentives, zoning amendments, and expedited permitting processes to encourage adaptive reuse. These policy tools can meaningfully alter project economics, but they vary widely in scope and effectiveness across jurisdictions.

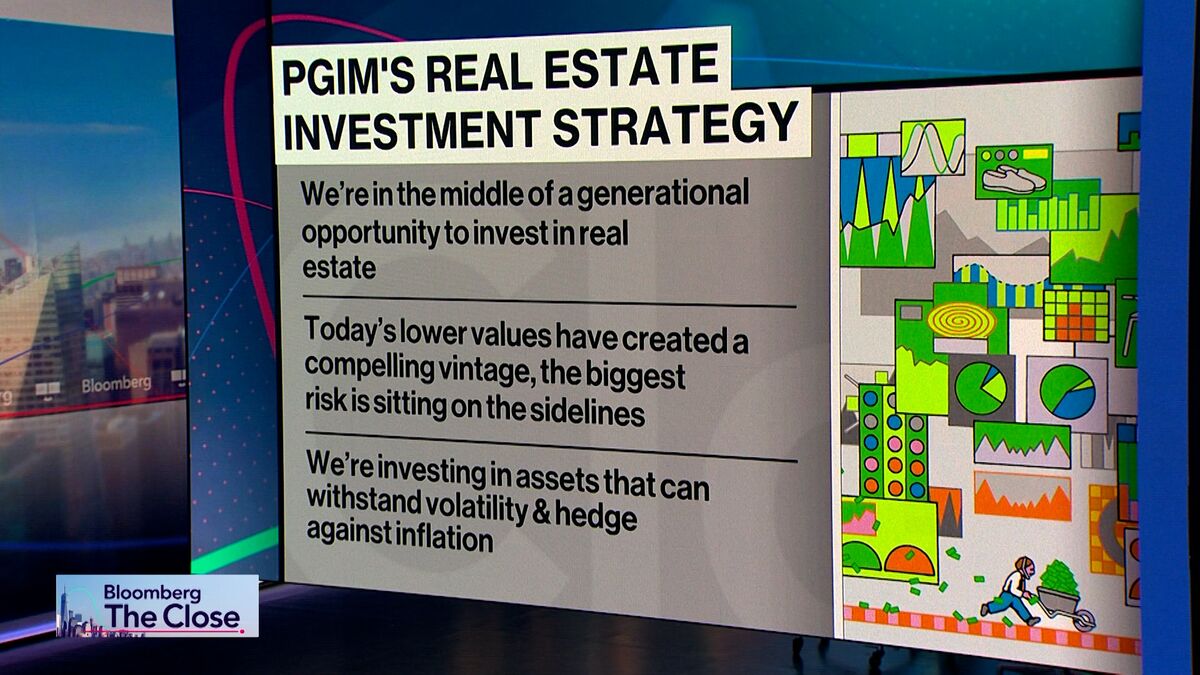

The broader strategic question for institutional investors like PGIM — which manages one of the largest real estate portfolios globally — is how to allocate capital across asset classes when two of the most compelling demand stories pull in different directions. Data centers offer high returns but face supply-side bottlenecks. Residential conversions address a deep societal need but carry execution risk and depend on local regulatory environments.

What makes the current moment distinctive is not that either trend exists in isolation, but that they coexist within the same capital allocation framework. The infrastructure limits of one asset class create pressure — and opportunity — in another. Whether the pace of office-to-residential conversion accelerates enough to meaningfully dent the housing deficit, or whether it remains a niche strategy confined to favorable building types and cooperative municipalities, depends on variables that neither market participants nor policymakers fully control.

With reporting from Bloomberg — Technology.

Source · Bloomberg — Technology