Mexico ranks among the world's largest automobile manufacturers, a position built over decades of investment, trade integration, and proximity to the United States market. Its factories now produce electric models for major global brands, including the Ford Mustang Mach-E. Yet the core technology inside those vehicles — the lithium-ion battery cell — arrives from overseas. Four years after a reform to the Mining Law declared lithium a national heritage and placed its exploration and exploitation under exclusive state control, Mexico has not produced a single domestically manufactured battery cell at commercial scale.

The 2020 legislative reform was framed as an exercise in resource sovereignty, part of a broader trend across Latin America in which governments sought to assert control over critical minerals tied to the energy transition. Bolivia had pursued a similar path with its vast lithium deposits in the Salar de Uyuni; Chile had long maintained partial state control over its reserves through Codelco and SQM. Mexico's move was distinctive in its absolutism: private concessions for lithium were effectively foreclosed, and a new state entity was tasked with managing the resource. The ambition was clear — to ensure that the economic value of lithium accrued domestically rather than being extracted by foreign capital. The execution, however, has lagged behind the rhetoric.

From Ore to Cell: The Missing Industrial Layer

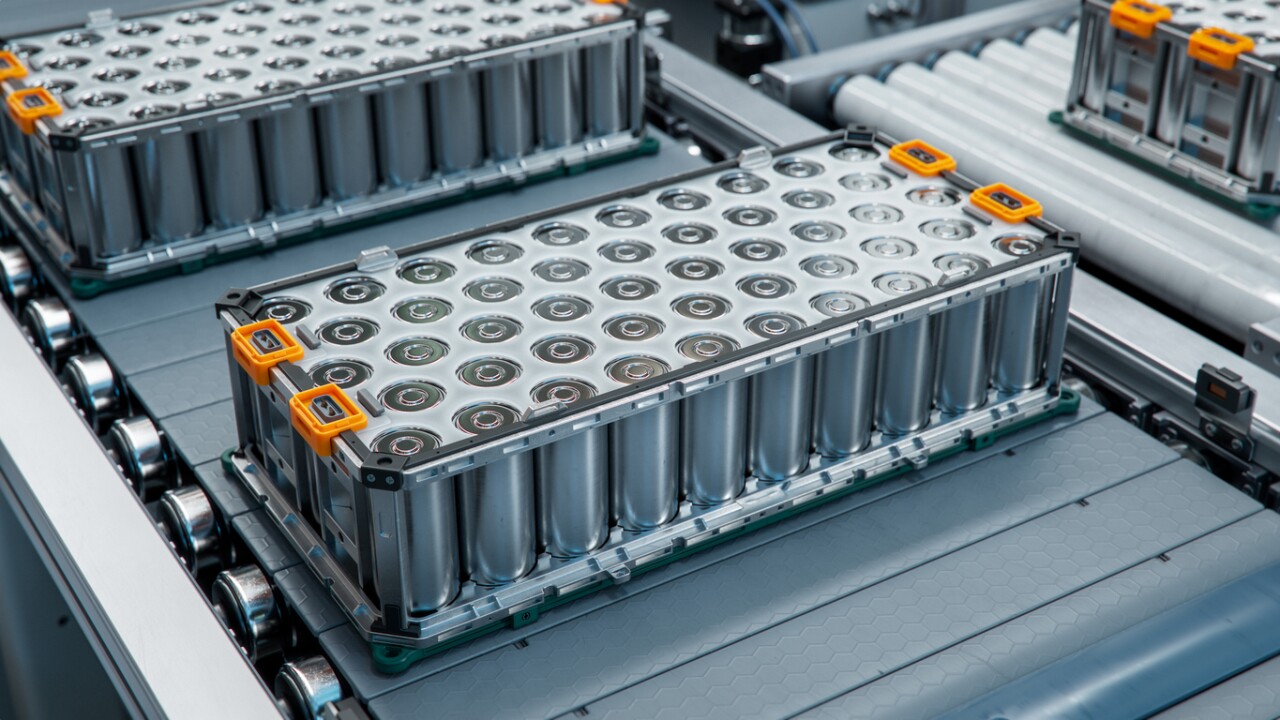

The gap between possessing lithium reserves and manufacturing battery cells is vast. Lithium must first be extracted — either from brine pools or hard-rock deposits — then refined into battery-grade lithium carbonate or lithium hydroxide, a process that demands specialized chemical engineering and significant capital. Only then can it enter the cell fabrication stage, where cathode and anode materials are assembled into the electrochemical units that store energy. Each step requires distinct infrastructure, technical expertise, and supply chain relationships that take years to develop.

Mexico's current industrial base covers the final stage of the battery value chain: pack assembly. Factories can take imported cells, arrange them into modules, integrate battery management systems, and install them in vehicles. But the upstream steps — refining and cell manufacturing — remain absent. Rodolfo Osorio, head of electromobility at the Ministry of Economy, recently acknowledged that it is "difficult to know exactly when" domestic battery production will begin. Research efforts at technical universities and institutes are underway, but the distance between laboratory-stage lithium processing and commercial-scale cell production is considerable.

This is not a uniquely Mexican problem. Indonesia, which controls a significant share of global nickel reserves essential to certain battery chemistries, has spent years trying to move beyond raw material exports into downstream processing, with mixed results. The battery cell manufacturing industry remains heavily concentrated in East Asia, where companies in China, South Korea, and Japan have built decades of process knowledge and supply chain density that newcomers cannot easily replicate.

Sovereignty Without Capacity

The tension at the heart of Mexico's lithium strategy is structural. Nationalizing a resource secures legal ownership but does not, by itself, create the industrial capacity to use it. Private investment — both domestic and foreign — typically provides the capital and technology transfer needed to build complex manufacturing operations. By restricting private participation in lithium, Mexico may have inadvertently slowed the very development it sought to accelerate. The state entity responsible for lithium has yet to demonstrate the operational capability or funding to advance extraction projects to production stage.

Meanwhile, Mexico's automotive sector continues to deepen its integration into the electric vehicle supply chain on terms set elsewhere. Battery cells arrive from gigafactories in the United States, China, and South Korea. The value captured domestically is real — assembly jobs, logistics, engineering — but it remains partial. The highest-value segment of the EV supply chain, cell manufacturing, generates margins and strategic leverage that pack assembly does not.

Mexico sits on lithium reserves, operates a world-class automotive manufacturing base, and has declared the mineral a matter of national patrimony. What it lacks is the industrial bridge between the first two assets — the refining plants, the cell fabrication lines, the trained workforce, and the capital commitments that would close the loop. Whether that bridge can be built under the current framework of state exclusivity, or whether some accommodation with private capital becomes necessary, remains the central unresolved question of Mexico's battery ambitions.

With reporting from Expansión MX.

Source · Expansión MX