The global energy landscape reached a quiet but profound inflection point in 2025. According to the latest annual review from the thinktank Ember, renewable energy has officially overtaken coal to become the world's largest source of electricity. It is the first time since 1919 that renewables have held a larger share of the power mix than coal, marking the end of a century-long era defined by the dominance of the so-called king of fossil fuels.

Unlike previous year-on-year declines in fossil fuel generation, which were typically the byproduct of economic recessions or global crises, the 0.2% drop recorded in 2025 appears to be structural. Wind and solar alone met 99% of the growth in global electricity demand last year. This suggests that the transition is no longer a matter of policy ambition alone, but a fundamental realignment of the world's industrial machinery.

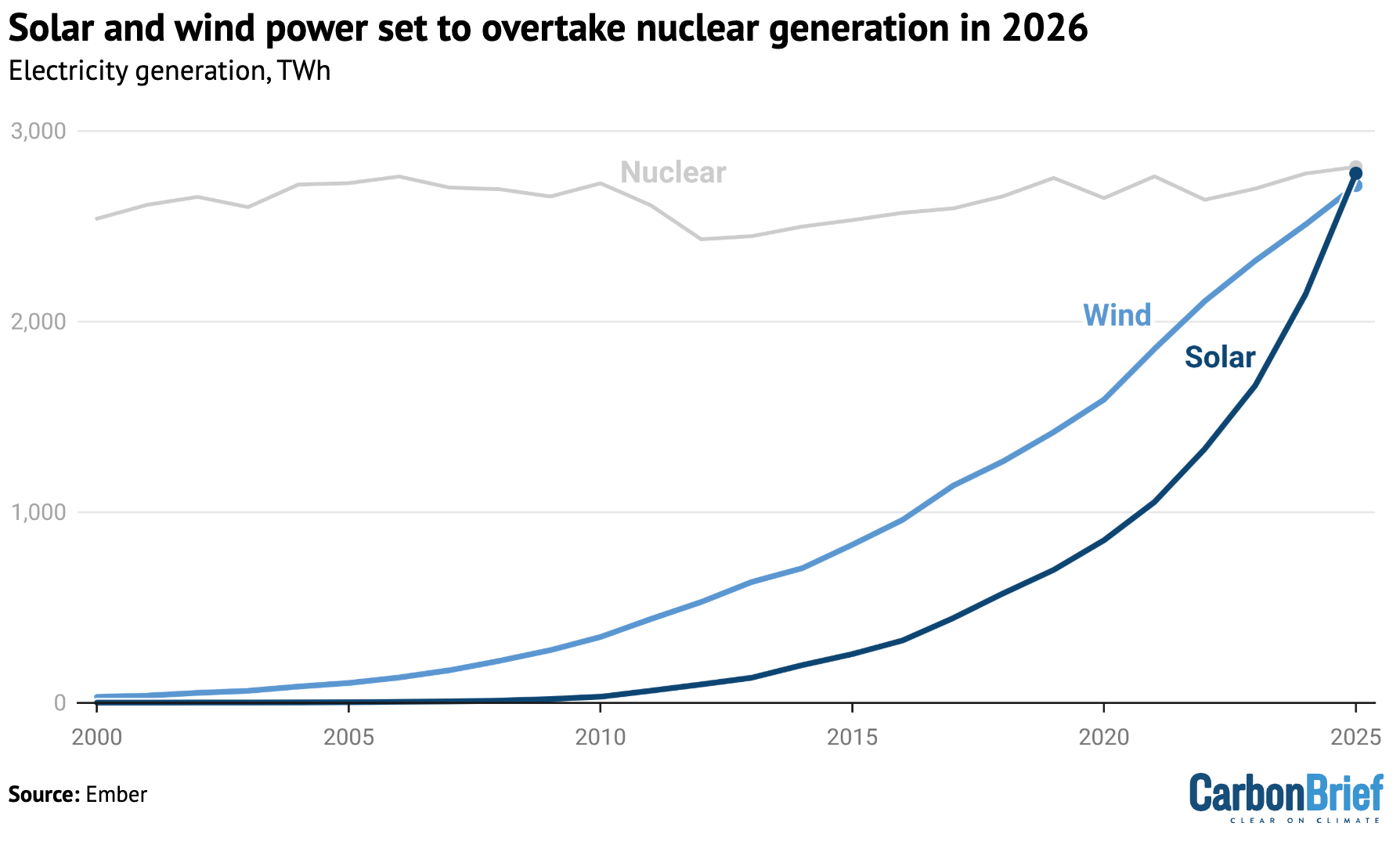

The solar engine and its scale

Solar power has emerged as the primary driver of this shift. Generation increased by 30% in 2025, meeting three-quarters of the entire global growth in electricity demand. The record 636 terawatt hours added by solar last year exceeded the total potential energy of all liquefied natural gas exports passing through the Strait of Hormuz — a comparison that underscores how rapidly solar has moved from a marginal technology to a force that rivals the output of critical fossil fuel chokepoints.

The trajectory is worth examining in historical context. A decade ago, solar accounted for a small fraction of global generation, often dismissed as too intermittent and too expensive to compete at scale. The collapse in photovoltaic module costs — driven largely by manufacturing expansion in China and incremental efficiency gains across the supply chain — has rewritten that calculus. Solar is now the cheapest source of new electricity generation in most markets, a fact that has shifted investment flows and reshaped grid planning across both developed and developing economies.

Meanwhile, the rise of electric vehicles has begun to erode the oil sector's foundations, displacing 1.8 million barrels of demand per day. This parallel erosion of oil demand, while still modest relative to total global consumption, signals that the electrification of transport is compounding the pressure on fossil fuels from both the supply and demand sides of the energy equation.

What structural means — and what it does not

The distinction between a cyclical dip and a structural decline matters. Previous drops in fossil fuel generation — during the 2008 financial crisis, or the demand collapse of 2020 — were followed by rebounds. The 2025 data, as Ember's analysis frames it, is different: clean energy growth is now sufficient to absorb new demand without requiring additional fossil fuel capacity. That is a threshold, not a fluctuation.

Coal now accounts for less than a third of global electricity generation for the first time in recorded history. Yet the structural pivot carries its own set of tensions. Grid reliability in systems with high renewable penetration depends on storage, transmission infrastructure, and flexible backup capacity — areas where investment has lagged behind generation buildout in many regions. The intermittency of wind and solar remains a technical constraint that battery storage and demand-side management are only beginning to address at scale.

There is also a geographic asymmetry. Much of the renewable capacity added in recent years is concentrated in China, Europe, and parts of North America. Emerging economies in South and Southeast Asia, where electricity demand is growing fastest, still face financing constraints and grid limitations that slow the adoption curve. Whether the structural pivot observed at the global level translates into a universal pattern — or remains unevenly distributed — will shape the pace of decarbonization for the next decade.

The data from 2025 confirms that the era of fossil fuel growth in the power sector has likely moved into the rearview mirror. But the road ahead is not simply a matter of extending current trends. The forces now in tension — accelerating renewable deployment against grid modernization needs, falling technology costs against rising mineral supply constraints, global ambition against uneven local capacity — will determine whether this inflection point becomes an irreversible turning point or a plateau that proves harder to move beyond than the initial breakthrough.

With reporting from Carbon Brief.

Source · Carbon Brief